GSDM Platform Seminar

Trend in Global Energy Supply and Demand, and Its Implications for Japan and Asia

Report

| [Date] | Monday, April 21, 2014, 13:30-15:00 |

|---|---|

| [Venue] | Ito Hall, Ito International Research Center, Hongo Campus of the University of Tokyo |

| [Hosted by] | Global Leader Program for Social Design and Management (GSDM), the University of Tokyo Graduate School of Public Policy (GraSPP), the University of Tokyo |

| [Co-Hosted by] | UTokyo Policy Alternatives Research Institute (PARI) |

Keynote Speaker: Dr. Fatih Birol

Chief Economist, International Energy Agency (IEA)

The current trends in the global energy picture and its implications for Japan were outlined by Dr. Fatih Birol as follows.

The roles of key actors in the current global energy scene are changing now. This means, firstly, that countries such as the United States which were energy importers in the past are now becoming energy exporters. Until recently, the US was the largest energy importer in the world, but due to the shale revolution, it is becoming a major exporter. Secondly, countries which were major energy exporters, such as Middle East, are becoming major energy consumers. In the last 5 years, their contribution to global oil demand growth is second only to China. Thirdly, there is a big change in how energy is traded between countries; for example, Canada is searching for new customers for their oil and gas in the Asian region since the US no longer imports oil and gas from Canada. Another example is the UAE, a major oil exporter in the Middle East, that now wants to import American natural gas. Hence, the shale gas revolution has changed many things, and companies who want to position themselves in advantageous ways need to understand these new energy realities.

On the other hand, there are several issues that have remained constant, but when changes are desirable. Firstly in this regard, CO2 emissions continue to increase. As a result, the world is moving towards a 4-degree global rise in temperature which will have devastating global consequences. Secondly, in emerging countries, fossil fuels are still heavily subsidized, resulting in inefficient usage and a growth in fossil fuel demand in those countries. Thirdly, about 20% of the global population still lives without electricity, especially in Sub-Saharan Africa and South Asian countries.

Regarding energy prices, there has been sustained period of high oil prices without parallel in history. $100 is becoming the new normal for oil prices, which is putting pressure on the trade deficits of many countries. Additionally, there are big regional price differences between natural gas and electricity. This means an increasing burden on the global competitiveness of countries like Japan

In terms of future energy demand growth, the trend has been increasingly moving towards Asian countries, especially China, and from 2020 onwards towards India. However, Chinese demand will taper off due to its slowing economy and a decrease in population growth. Interestingly, it appears that the Middle East is presently also becoming a major energy demand center.

Looking at the global energy mix, 25 years ago fossil fuels accounted for 82% of energy consumption, and despite all the efforts of various agencies to bring this share down, today it still stands at 82%. This shows that economic facts are stubborn and more often than not belie government statements. However, even in the future, fossil fuels, especially natural gas, will still dominate the global energy markets, generally because of government subsidies. If those subsidies are removed, as is presently being seen in Europe and elsewhere, growth in renewable energy may increase.

The US and the success story of the shale revolution which started around 7 years ago is a noteworthy case. Today, US shale gas production is equivalent to the total production of Qatar, Kuwait, the UAE, and Iraq combined. US shale oil production has reached 3 mb per day within the last 7 years, equaling Iraq's entire oil output. This has given a new dimension to the US's energy position and its foreign policies, as well bringing other considerations to the fore.

In the past, one major topic of US presidential elections used to be whether the US could be self-sufficient in terms of oil some day. World Energy Outlook 2013 shows that the US may indeed be self-sufficient in oil very soon. This is still a hot topic in US public policy today. There are two major reasons that account for US progress toward self-sufficiency: the first is increased oil production due to shale oil, and the second is reducing domestic oil demand stemming from the adoption of policies that improve vehicle efficiency. These policies were mainly adopted during the first Obama administration.

However, it should be noted that since the US has high domestic oil needs, it can never be a major oil exporter in the future. Hence, any assumption that US may end its reliance on Middle East production in the future is entirely misguided. From 2020-2025, US oil production will increase, but will soon fall behind demand. After that, the world will need oil from the Middle East, especially to meet large growth in demand from Asia; only the Middle East has capacity to meet that oil demand. Hence, the Middle East should not get the wrong message that its oil will not be needed in the future.

The US shale revolution brings several advantages, one being a decrease in CO2 emissions. Until 2007, US CO2 emissions were increasing every year, but as shale gas production increased in 2007, emission levels declined significantly since shale gas was replacing coal. This is good news for climate change. However, the truth is that the US started using more shale gas for purely economic reasons, simply because it is cheaper than coal. This important fact should not be forgotten because in 2013, with an increase in the shale gas price, coal is once again a marketable commodity with the result that United States' CO2 emissions levels have started increasing again. Unless the Obama administration is successful in putting a regulatory ban on coal-fired power plants, if gas prices continue to increase, then coal consumption in the US will steadily rise, along with CO2 emissions.

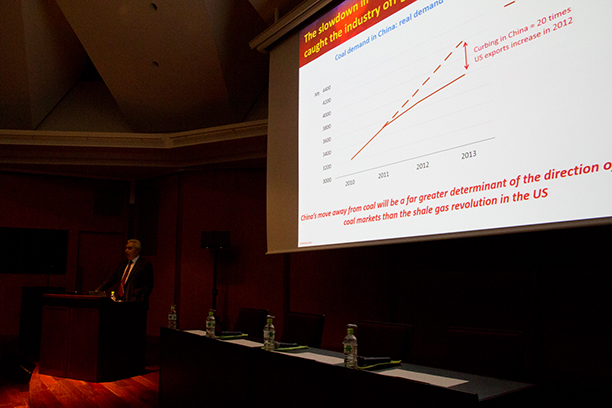

In the last few years, a major development has been that globally coal prices saw a large drop, falling from over $100 to $75. Many people wrongly thought this was because US was exporting coal. However, the data shows that the US was a minor culprit. Indonesia contributed hugely to the growth of coal exports and even Australia, though to a lesser extent, contributed to the expansion. Additionally, in the last few years, Chinese coal consumption has slowed down substantially. The difference between historical coal consumption and current real coal consumption by China is 20 times higher than US coal exports.

Before the shale gas revolution, natural gas prices in different regions were similar, but after the shale revolution, there has been a huge difference in gas prices, with European gas prices standing three times higher than the American price, while the Japanese gas price stands fully five times higher. The most worrying news for Japan and Europe is that this is a structural issue which may last for many years. The same applies as well to electricity prices. This means Japan will remain a high energy cost country for many years, which will put Japan at a major economic disadvantage compared to the United States, Middle Eastern Countries, and others. Looking at the international trade generated by energy-intensive industries in the future, countries such as the US, China, and the Middle East look to be clear winners whereas Europe and Japan come out as losers due to their higher energy costs. In this regard, it should be pointed out that people were completely wrong to think that if US exported its cheap gas to Europe and Japan, then gas prices would decrease and the problem would be solved. The reasons being that after adding the costs of liquefaction, shipping, and regasification to the import price, the cost of gas would rise to a level almost equal to what it is already in these countries. Hence, large gaps in gas prices between global regions will remain in the future.

Focusing on the Japan energy issue, the impact of a zero nuclear policy for Japan should be further deliberated. Firstly, since Japan will not produce electricity from nuclear power, this will have to be compensated for by other fuels, which will put an additional ¥1.3 trillion burden per year on the Japanese economy. Secondly, Japan needs to build a new LNG terminal and power plants to compensate for the loss of nuclear power. This will need an additional investment of $250 billion per year. As a result, Japan's energy self-sufficiency will hugely deteriorate since it will have to rely on imports from other countries. Additionally, Japan's increased demand for LNG would put increased pressure on LNG prices in Asia. There will also be major climatic implications for Japan in using LNG or coal. If Japan insists on a zero nuclear policy, CO2 emissions would then be even higher than in the year following the Fukushima disaster.

In concluding the keynote speech, the following points were emphasized:

- There are significant regional price gaps across the globe resulting in concerns over competitiveness for countries such as Japan. To neutralize some of the negative effects for such countries, energy efficiency policies must take priority.

- Gas coming from America can narrow this regional price gap only to a limited extent. Because of transportation and other costs this gap will not narrow significantly.

- Nuclear power and renewables can contribute to energy security, climate change goals, and enhance energy competitiveness.

- Schemes to support renewables are desirable, but such projects need to be carefully evaluated for viability and cost-effectiveness.

- The new Basic Energy Plan of Japan sends a strong message about Japan's commitment to delivering reliable, secure, affordable, and clean energy. To gather support for this plan, the Japanese public, together with academics and policymakers need to discuss these important issues through forums such as UTokyo PARI.

Prof. Ryuji MATSUHASHI

Department of Electrical Engineering and Information Systems, Graduate School of Engineering, the University of Tokyo

Moderator: Prof. Hisashi Yoshikawa

Policy Alternatives Research Institute (PARI) / Graduate School of Public Policy (GraSPP), the University of Tokyo

Cooperation between countries and regions principally helped in improving flexibility and economies of scale through cost reduction. Choosing the right neighbors and partners could definitely be a solution for cost reduction and diversity for energy supply security, but this choice is a difficult one. However, theoretically, such cooperation is indeed feasible as evidenced by the pool of Nordic countries that profit from their connections.

It was mentioned that while 30 years ago IEA countries accounted for two-thirds of oil consumption, this has decreased to half presently, and it is expected that IEA consumption will soon reduce to one-third. Hence, the relevance of IEA countries in the oil market is declining while the relevance of India, China, and the Middle East is increasing due to their growing oil demand. If the IEA wants to remain relevant, then these emerging countries should be admitted to the club.

Prof. Hideaki Shiroyama

Dean, Graduate School of Public Policy / Professor, Graduate Schools for Law and Politics & Policy Alternatives Research Institute (PARI), the University of Tokyo

It is undeniable that while economic growth does not necessarily guarantee happiness, poverty is its antithesis. Economic welfare and financial security provide the foundations that underpin people's happiness. It is agreed that the issue of happiness is not germane to the debate over nuclear power. In fact, safety and public acceptance should come first, but we should not forget to consider the future and prosperity of Japanese citizens and that, in this regard, Japanese citizens would be much happier given economic prosperity.

To conclude the discussion, the fact that today energy is at the heart of many things was greatly emphasized. Energy is related to climate change, the economy, and public policymaking. Finally, Dr. Birol congratulated the organizers for establishing the GSDM program. Such interdisciplinary discussion focusing on energy is vitally important, he said, and for those aiming at leadership positions participation is a must.

Related Links

GSDM (Global Leader Program for Social Design and Management), the University of Tokyo

Global Energy Policy and East Asia Research Unit